"If you have a financial plan that does not contain an adequate amount of Disability Income Insurance, you don't have a plan... you are a circus act without a safety net!" -- Jane Bryant Quinn

"Who needs disability insurance? Everyone! You should have long-term disability insurance regardless of what job you have..." – Dave Ramsey

Your income determines your lifestyle, but if you become even temporarily disabled, are you protected against a drastic change in your standard of living? Your ability to work and earn income is your most valuable asset. You probably have protection for the things your income makes possible i.e., your car and your home. But have you protected your greatest asset from the risk of an unexpected accident or sickness? Disability Income Insurance replaces part of your income if you are ever too sick or injured to work.

Eisenberg Associates offers:

The cost of a long term disability is not easily measured. How do you measure the loss of educational opportunities, the cost of shattered lives, altered personalities? How do you measure the cost to society when boys and girls who are potential doctors, lawyers, architects, teachers or scientists are denied the opportunity for training because their fathers became disabled and were unable to finance the necessary education? How do you measure the cost of heartbreak when the family's treasured possessions must be sold? How do you measure the cost when a dynamic individual has lost all initiative and hope?

The cost of disability can be so high that it can't be measured, or it can be minimal. The cost can be limited to the amount of dollars required to provide adequate income protection plus the inevitable discomfort and physical pain that accompanies the disease or injury. However it is paid, the cost is inescapable. The cost will be paid in loss of savings, loss of homes, loss of pride, humiliation, shattered plans and shattered lives. Or, it will be paid the easy way, through payment of premiums on a disability income policy.

A sole proprietor will pay the cost as his business and income fade away when he can't operate the business. A doctor will pay the cost as his practice goes elsewhere. An employer will pay the cost as he continues salary to a key person (and his/her replacement) or to a disabled partner. If death will cause a problem for a business, you can be certain that a long term disability will also extract a heavy price and additionally it is a devilish emotional problem never satisfactory to any of the partners. In every such case, however, the cost can be minimized through the means of an intelligently devised disability insurance program.

Resources:

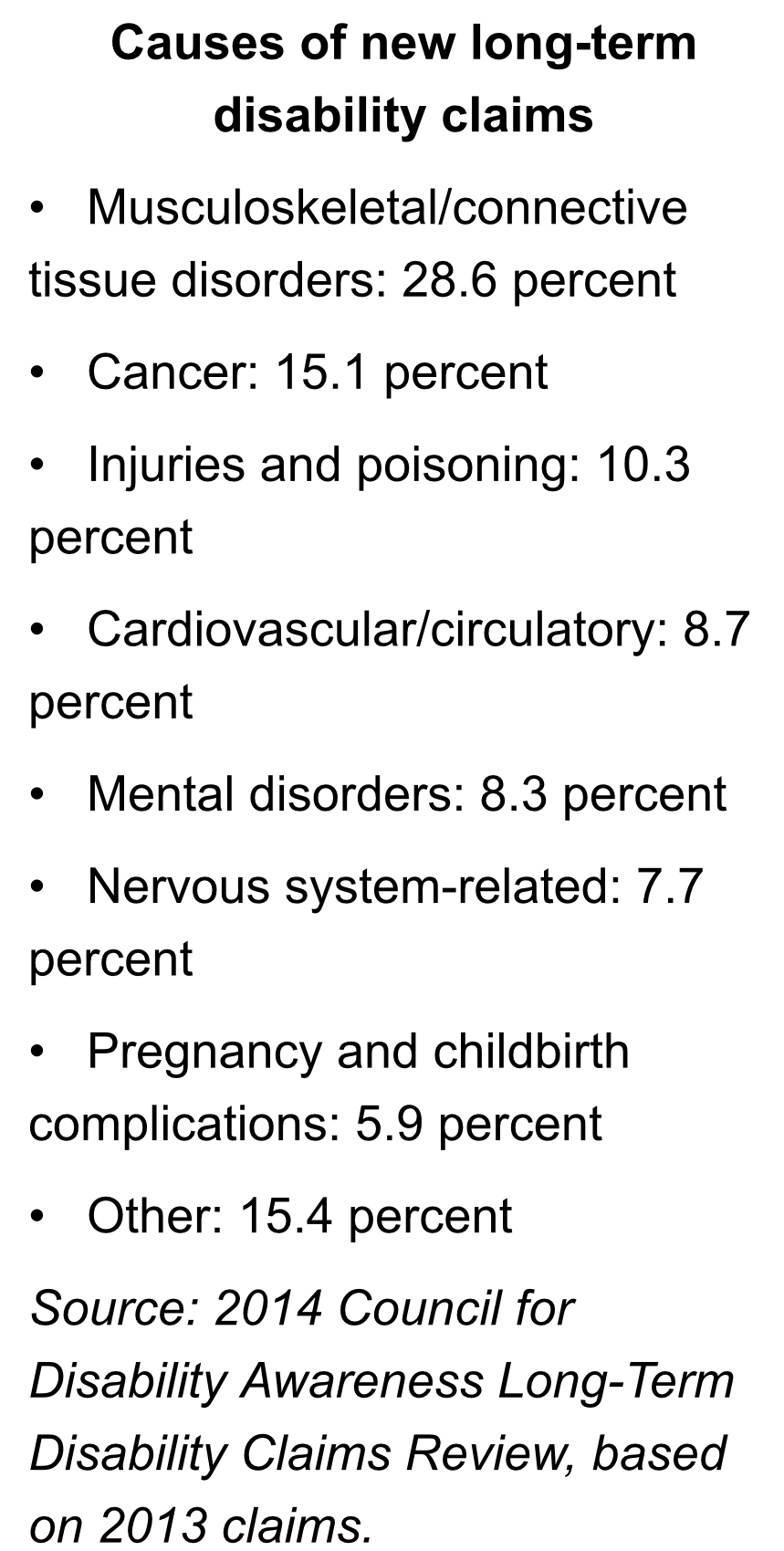

Can you guess how many people are currently disabled in America? This week? This month? This year?

The top reasons every working American needs paycheck protection